Italian Leather Machinery Isn't Dying — It's Been Filtered

- alessandro5941

- May 19

- 4 min read

Every year Assomac publishes its sector report. This year's numbers will be read wrong by anyone who stops at the surface. Italian leather-machinery companies down from 400 to 225 in thirty years. Revenue down 32%. Average ROE collapsed from 15.8% to 4.1% in seven years. Read like that, it sounds like an industry dying. Read inside the balance sheets of the 225 survivors, it's something else entirely — and what it means for your plant in 2026 is the part nobody is talking about.

What the numbers actually say

The headline reads as collapse. 400 to 225 companies. 7,200 to 3,800 employees. Revenue from €842M to €575M between 1996 and 2024. But inside the balance sheets of those 225 survivors, something else is happening: equity ratio from 47% to 59%, debt-to-capital at historical lows, net equity +53% since 2015. The market has filtered the table for two decades. The companies still standing are leaner, less leveraged, and structurally healthier than they have been at any point in the last twenty years. This isn't an industry in agony. It's an industry that has already paid its selection bill. The question is what those survivors do next.

The volume game with China is over

In 2005 Italy held 42% of world leather-machinery exports. China was at 3%. In 2024: China 44%, Italy 31%. First half of 2025 widens the gap further — Chinese exports €270M against Italian €124M (Assomac data). The volume war for cheap machinery serving fast-fashion footwear in Vietnam, Indonesia, Bangladesh is lost. It isn't coming back. What is not lost is the value game. Italian top export destinations remain China, India, France, Brazil, Spain, Turkey — diversified, value-add markets where quality, service, and certification still pay a premium. Two different customers. Two different games. The first one we shouldn't keep playing, no matter how stubbornly.

The customer base has already split

Three Italian customer segments. Same country. Same regulations. Three completely different industries.

Italian tanning lost 50% of m² production since 1996. Italian footwear lost 74% of pairs produced. But Italian leather goods went from €2.2B to €12B in production value, driven entirely by global luxury concentrating its manufacturing in Tuscany. If you're a machinery supplier, the customer who was there in 1996 doesn't exist in the same form anymore. Luxury leather goods has different specs, different cycles, different quality bars from volume tanning or volume footwear. The product roadmap has to follow.

"Pretending the customer is still volume tanning is the fastest way to misallocate the sales effort. The customer who was there in 1996 doesn't exist in the same form anymore."

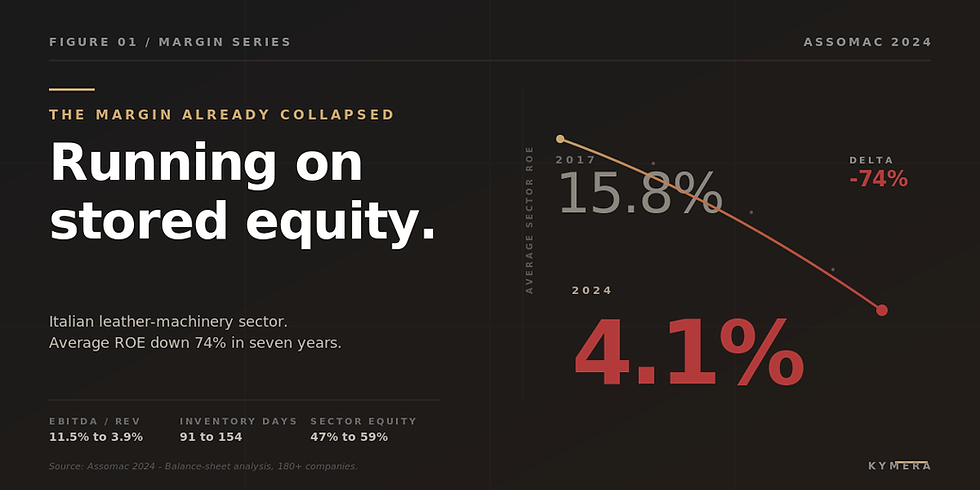

The real signal is in the margins

The volume story is loud. The margin story is the one that should keep anyone in this sector up at night. Average sector ROE: 15.8% in 2017 to 4.1% in 2024. EBITDA/Revenue from 11.5% to 3.9%. Labor cost over revenue climbed from 19% to 27%. Inventory days from 91 to 154 — warehouses full of stock that isn't moving. Net profit nearly halved versus 2017-2018. Translation: the survivors are not earning their living. They're spending what they saved. That position holds for a while. It does not hold forever. By 2027-2028, the equity buffer thins out for many of these companies, and the question of what they sell next becomes operational, not strategic.

What this means for your plant in 2026

Three operational reads — not opinions, observations from twenty years inside this sector.

**Stop competing on volume.** If the business model still depends on shipping low-margin equipment to volume tanneries or volume footwear, the next five years will hurt. The customer is leaving the segment, not the machinery.

**Position around luxury leather goods.** It's the only Italian customer segment in real growth. Precision, repeatability, quality control — everything Italian machinery still does better than China at the high end.

**Move value from selling to servicing.** Reblading, spare parts, software, after-sales, customer financing. These are parts of the business China can't replicate at zero cost — they require physical presence and relationship years.

This is the logic we built Kymera around.

The machine itself is never the starting point. It's the outcome of understanding the plant — what the line actually needs, what budget fits, what the customer can absorb operationally. New, reconditioned, or used: that's a consulting decision, not a product pitch.

Spare parts and post-sales — spare parts, consumables, service, on-site intervention, T-CAT Pro for tannery management — are where we stay close to the line, every week. Not transactions. Relationships.

On payments: KEP (Kymera Easy Pay, our rotating credit line) and crypto acceptance are tools to remove friction. In a sector where the real problem is cash flow — not machine spec sheets — that matters more than discounts.

The Assomac 2024 numbers are tough. But they describe an industry that has already filtered itself, and that now needs to decide whether to accept a different game than the one of the last thirty years. Anyone still playing yesterday's game leaves the table within five. Anyone who accepts the game has changed still has everything to build.

--------------------------------

Written by Alessandro Burlando, founder of Kymera Group. 20+ years in tannery machinery and consumables. If you want to compare notes on what this means for your plant, message me on LinkedIn or WhatsApp +39 320 573 1618.

Comments